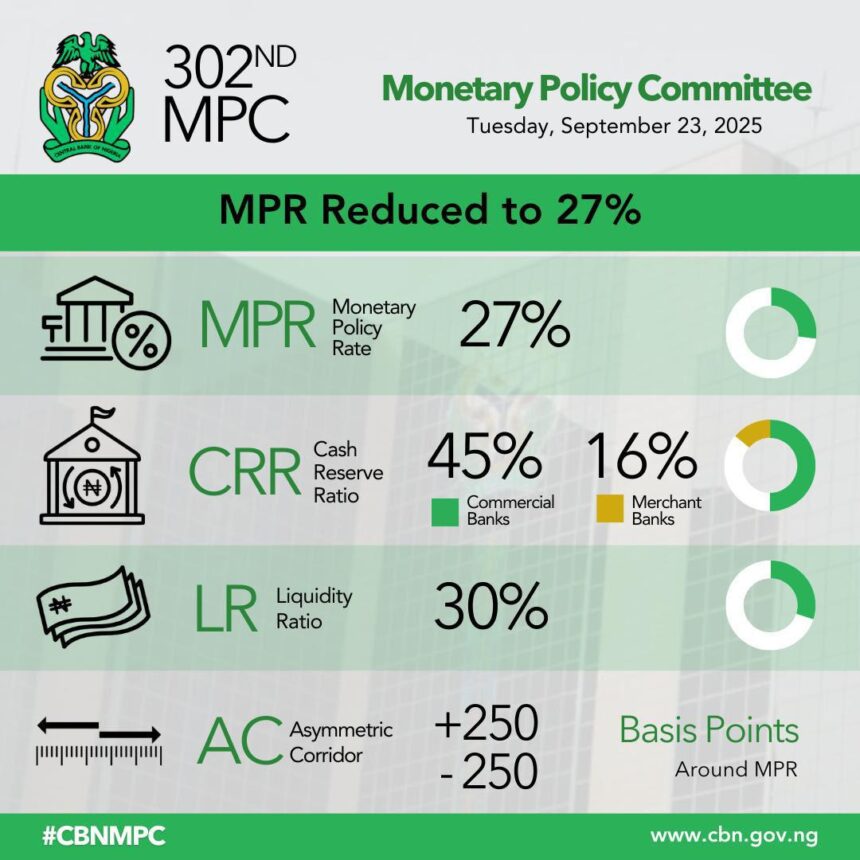

The Central Bank of Nigeria (CBN) has taken its first step towards easing monetary conditions in months, cutting the Monetary Policy Rate (MPR) by 50 basis points to 27.0%. The decision, made at the latest Monetary Policy Committee (MPC) meeting, signals a cautious attempt to support credit growth while still keeping inflation and currency pressures in check.

Key Policy Changes

MPR: Down 50bps to 27.0% — a small but symbolic reduction in borrowing costs.

Asymmetric Corridor: Left unchanged at ±250bps, keeping overnight rates between roughly 24.5% (deposit window) and 29.5% (lending window).

Cash Reserve Ratio (CRR): Cut by 500bps to 45% for commercial banks, unchanged at 16% for merchant banks.

Liquidity Ratio: Held steady at 30%.

New Rule: 75% CRR imposed on non-TSA public sector deposits, forcing banks to release idle government funds or focus more on private-sector deposits.

Implications for Businesses

While the rate cut is modest, the overall stance remains tight. Here’s what this means in practice:

Borrowing Costs: Expect a slight reduction in interest rates on MPR-linked loans (around 0.5%), though transmission may be slow.

Liquidity: Cash will remain expensive. Banks are unlikely to open the credit taps widely, so working capital funding may stay selective.

FX Market: The naira could face mild pressure, but the high CRR will keep excess liquidity in check, limiting currency volatility.

Capital Markets: Treasury bill yields may soften slightly, especially at the short end. Equity markets may see a valuation boost, but earnings and FX stability still matter more.

Action points for CFOs and finance teams

1. Reprice Loans: Update cash-flow and interest-cost projections using the new MPR. Confirm repricing timelines with lenders.

2. Optimise Treasury: Diversify T-bill investments across maturities (91-, 182-, 364-day) to manage reinvestment risk in case of further easing.

3. Plan working capital carefully: Maintain tight receivables management. Model interest expense at ±200bps scenarios to stay prepared.

4. Refresh budgets: Adjust weighted average cost of capital (WACC) assumptions for 2025 forecasts.

5. Update risk models: Incorporate new policy rates and liquidity expectations into IFRS 9 ECL calculations (PD/LGD models).

6. Board reporting: Present a balanced view — modest relief on costs, but still tight credit conditions.

Board summary:

“CBN has cautiously eased rates but continues to enforce tight liquidity controls. Corporates should expect small reductions in borrowing costs, no liquidity flood, and continued pressure to manage cash and credit efficiently.”

Bottom Line

This is a “soft pivot” — not a full-blown stimulus. Businesses should see gradual cost relief but must continue to plan conservatively, keep financing options open, and stay agile as the CBN walks the line between growth support and currency stability.

–